Part 3 - Jefferson County: "Stuck by Design"

Part 3 – How We Got Here

From pre‑COVID tightening to the “Zoom town” era and the interest‑rate shock that followed: the story of the last decade in plain language.

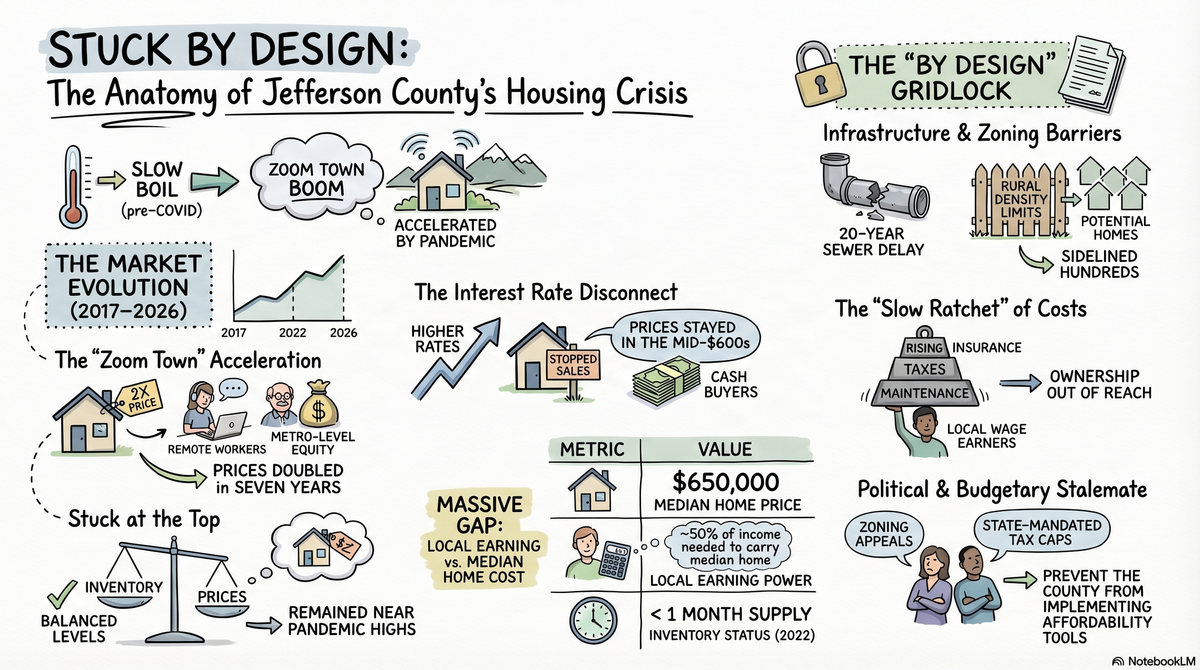

Before COVID hit, Western Jefferson County was already on a slow boil. Prices were rising faster than local paychecks, and the number of homes for sale was steadily shrinking. From the middle of the last decade through 2019, the median price climbed from the high‑200s into the low‑400s, even as active listings fell by roughly a third. The county formally declared a housing emergency for lower‑income households back in 2017, long before anyone had heard the word “COVID‑19.” The basic pattern was set: local wages couldn’t carry the market, but retirees, second‑home buyers, and commuters bringing Seattle‑area incomes and equity could.

When the pandemic arrived, it didn’t create a new story — it hit the fast‑forward button on the one already in progress. Jefferson County became a textbook “Zoom town” as remote work let higher‑income buyers cut the cord to big‑city offices and move to places like Port Townsend while keeping metro‑level pay. Between 2019 and 2022, prices jumped by roughly half, and the number of homes for sale collapsed to a level where the entire county had less than a month of inventory. Ultra‑low mortgage rates near 3% made buying feel cheap to these newcomers, and second‑home demand piled on as people sought private, scenic refuges during lockdowns. By mid‑2022, median home values had more than doubled in about seven years.

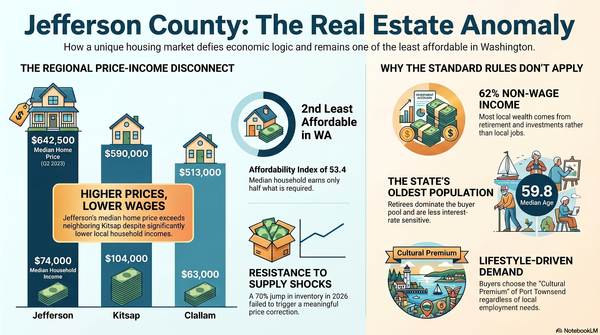

The interest‑rate shock that followed was supposed to be the cold shower. Starting in 2022, the Federal Reserve pushed benchmark rates from near zero to above 5%, and 30‑year mortgage rates shot past 7%. Transaction volume reacted exactly as the textbooks say: sales fell sharply from their 2021 peak, and many existing owners with 2–3% loans simply stopped listing, locked into place by their cheap debt. Affordability for mortgage‑dependent local buyers cratered. But prices barely flinched. Instead of falling, the median slid sideways to slightly up — still clustered in the mid‑600s. That disconnect is the heart of the “stuck” story. The marginal buyer in Western Jefferson County is often an equity‑rich retiree or remote worker paying cash or bringing a large down payment, so higher mortgage rates hit local wage earners hard but don’t fully register with the buyers who actually set the price points.

By 2025–2026, the market finally began to loosen — but in a way that shows just how deep the structural problems run. Active listings surged, posting some of the largest year‑over‑year inventory gains in the state. Months of supply moved into the 4–6 month “balanced” range for the first time since before the pandemic, and homes started taking far longer to sell. The median days on market more than doubled, and sellers began pricing more realistically and accepting offers a few percent below list — a sharp contrast to the bidding wars of 2021–2022. Yet prices remained within a couple of percentage points of their pandemic‑era highs, and the annual median still sat around $650,000 dollars. On paper, this looks like a market cooling off; in practice, it’s a market pinned in place — softer for sellers, but still out of reach for most local workers.

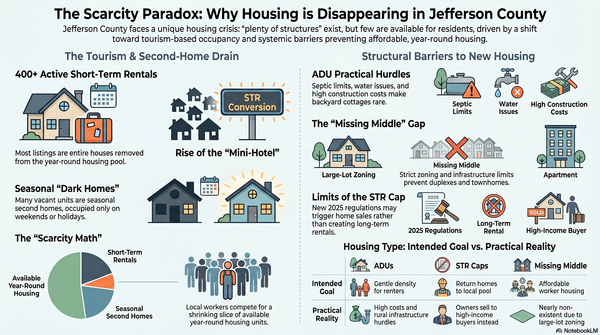

Underneath these swings is the “by design” part: policy choices that have quietly limited supply for decades. Washington’s Growth Management Act locks most of the county into very low rural densities — one house per five, ten, or twenty acres across the vast majority of the land — and generally forbids extending sewer into those areas. That leaves just two places where real urban‑scale housing can go: the City of Port Townsend and the Irondale/Port Hadlock Urban Growth Area. Port Townsend’s UGA boundary has barely budged since the early 1990s; only in the most recent plan cycle was a small expansion approved for a homeless services village. The Port Hadlock UGA, meanwhile, was given urban zoning on paper in the early 2000s but spent nearly two decades without the sewer needed to make those densities real.

Phase One of the Hadlock sewer is finally built and operational, but it only serves a core band of commercial properties. The surrounding residential areas — where new multifamily or smaller lots could actually take pressure off prices — remain on septic, and the next phases of sewer expansion are not fully funded. That long delay effectively sidelined hundreds of potential homes during the very years demand was exploding. In other words, when outside capital arrived in force, the only truly “legal” places to build new housing were already mostly built out, and the one big growth area on the map was stuck at rural performance because the infrastructure never kept pace with the zoning.

Local politics has reinforced the gridlock. In Port Townsend, many long‑time homeowners have organized against upzoning, height increases, and more flexible infill rules. Public hearings on the city’s comprehensive plan and zoning updates have been packed with opposition to sixplexes, taller buildings, and reduced parking, often framed around gardens, sunlight, views, and neighborhood “character.” Working renters and families — the people most affected by high prices — are largely absent from weekday hearings but vocal on social media. When the city finally adopted a more pro‑housing plan in late 2025, an opposition group immediately appealed it, tying up the Growth Management Hearings Board and city staff time that was supposed to go toward implementing density increases and affordability tools. That appeal is part of a longer pattern: delay, dilute, or block density reforms, even while declaring support for “affordability” in the abstract.

At the county level, other constraints reinforce the same “stuck” dynamic. The 1% cap on the regular property‑tax levy keeps the General Fund on a slow starvation diet, even as costs for public safety, planning, and infrastructure climb. The county now faces a chronic budget gap: without voter‑approved lid‑lifts or special levies, it must cut services or delay investments — including some that would make permitting faster or infrastructure more supportive of new housing. Yet each new levy or proposed rate increase lands on the same homeowners who are already stretched by high mortgage payments and ongoing cost increases. The result is a political stalemate: residents resist new taxes that would add to their monthly housing burden, while the same revenue constraints make it harder for local government to tackle the housing crisis meaningfully.

On top of that, there’s the slow ratchet of non‑mortgage housing costs that rarely show up in listing photos or headline statistics. Even if prices flatten and mortgage rates ease, the all‑in cost of owning a home continues to creep up through insurance, property taxes, utilities, and maintenance. Homeowners insurance, in particular, has been rising rapidly as construction costs, wildfire risk, and broader climate‑related losses filter through the system. In practice, that means the “other” line items on a buyer’s escrow statement grow by dozens of dollars a month over just a few renewal cycles. Property taxes follow a similar pattern: even with the levy cap, new voter‑approved measures and rising assessed values can nudge the annual bill up, especially on higher‑value homes.

You can see how this plays out for a typical Jefferson County buyer seeking a $650,000 home. The principal‑and‑interest payment is only the first layer. On top of that, property taxes add a few hundred dollars a month. Homeowners insurance adds another substantial line item, especially amid rising premiums. Basic maintenance and utilities — roof repairs, septic work, heating, water, and power — easily stack on top of both. What looked like a manageable mortgage when quoted in isolation turns into a total monthly cost that is hundreds of dollars higher than a buyer expected. Each of those pieces — taxes, insurance, utilities, upkeep — ticks upward over time. Together they form a slow ratchet that tightens around local households, even in a so‑called “cooling” market.

The result of all these forces is the housing market Western Jefferson County lives with today: prices that reflect metro‑area and retirement‑market money; a construction pipeline throttled by zoning, sewer, and politics; a county budget constrained by state‑level caps; and a local wage base that simply can’t bridge the gap. The formal affordability metrics capture the outcome — a median household that earns only about half of what it takes to carry the median home — but not the lived experience of how we got here. Pre‑COVID tightening set the stage, the Zoom‑town era delivered the shock, the rate hikes exposed just how little room there is for the market to self‑correct, and the slow ratchet of ongoing costs keeps pushing ownership further out of reach. This isn’t a market that’s crashing; it’s a market that’s stuck by design.