Part 4 - Jefferson County: "Stuck by Design"

Part 4 – Affordability and Who Can Buy

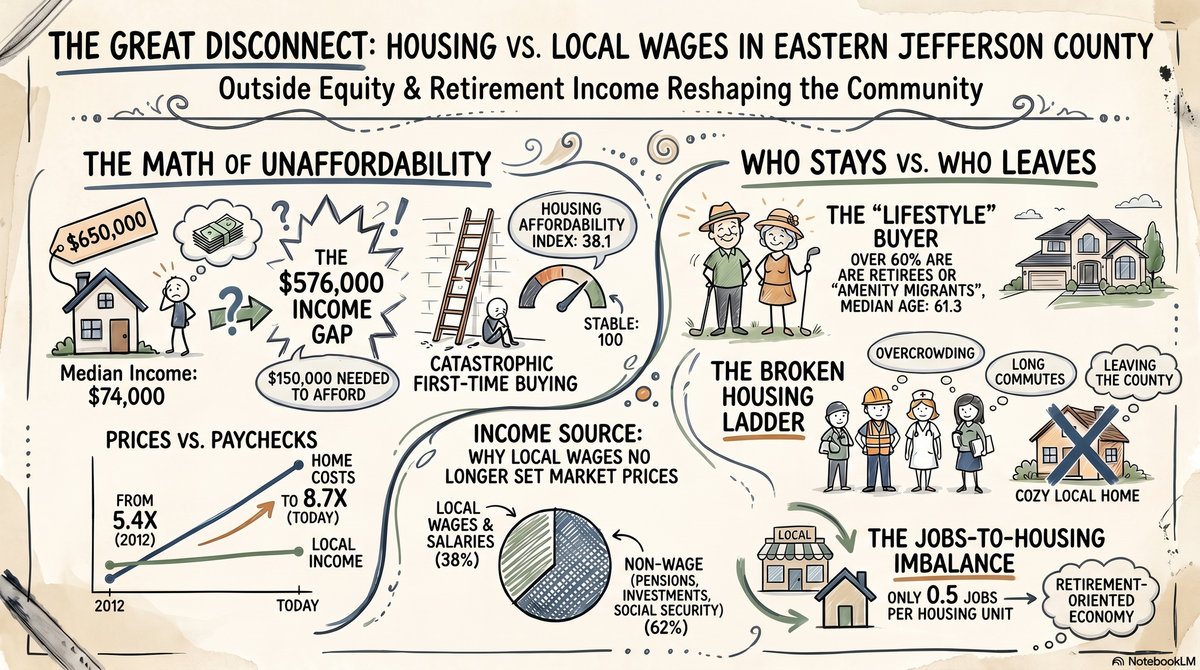

Eastern Jefferson County’s housing market no longer runs on what local work pays. Prices are now set by people bringing in outside equity and retirement income, and that shift is deciding who gets to move here, who can stay, and who quietly leaves.

The math: prices vs. paychecks

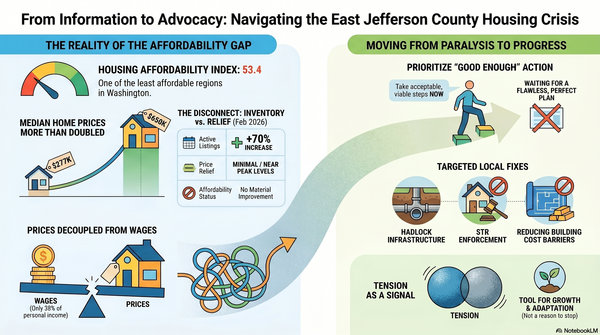

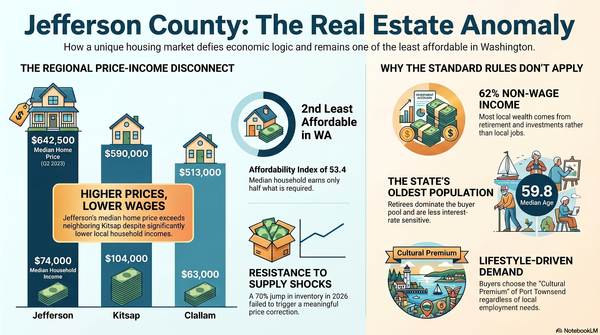

On paper, the story looks simple. In 2025, the countywide median home price was about $650,000, while the median household income was roughly $74,000. At recent mortgage rates and tax levels, you need on the order of $150,000 in annual income to comfortably buy that median home, and around $84,000 to afford the average market rent of $2,091 per month without being stretched thin.

The Housing Affordability Index (HAI) turns that gap into a single number. An HAI of 100 means a median household earns exactly what’s needed to qualify for the median home. Eastern Jefferson County’s HAI is 53.4, which means the typical household earns just 53 percent of what a conventional lender would require. For first‑time buyers, the index drops to 38.1—a level housing researchers describe as “catastrophic” unaffordability.

Over the past decade-plus, the relationship between prices and incomes has drifted out of orbit. Around 2012, the median home cost about 5.4 times the median household income; today that ratio sits closer to 8.7. That is higher than in some major job centers, which is remarkable in a rural county with no large corporate employers and a modest local wage base.

Who can actually buy here now?

When you line up those numbers, a pattern emerges about who can buy. Market analytics show that more than 60 percent of Eastern Jefferson County homebuyers fall into two lifestyle‑driven segments—“Golden Years” and “The Great Outdoors”—which are essentially retirees and amenity migrants seeking small‑town culture and natural beauty. The median buyer age is 61.3, making this fundamentally a retirement and lifestyle market rather than an employment-driven one.

Income data backs that up. Only about 38 percent of total personal income in the county comes from wages and salaries, compared with roughly two‑thirds statewide. The remaining 62 percent comes from non‑wage sources: Social Security, pensions, investment returns, and transfer payments. In practical terms, that means many buyers are tapping home equity earned elsewhere, retirement portfolios, or remote jobs tied to higher metro pay scales.

That changes how this market responds to interest rates. For a local household trying to stretch a $90,000 combined income into a purchase, a 7 percent mortgage rate can be the difference between owning and being permanently sidelined. For a retired couple arriving with $700,000 in sale proceeds from Seattle or the Bay Area, or a remote worker making six figures, a $650,000 home in Eastern Jefferson County still looks achievable—especially if they can pay cash or make a very large down payment.

Meanwhile, the local job base remains small and tilted toward modestly paid sectors. The county has just under 9,000 covered jobs, heavily concentrated in government, retail, hospitality, and health care. The paper mill’s roughly 300 jobs at around $92,600 per year are the exception, not the norm, and tourism’s 1,300 direct jobs are vital but often seasonal and lower‑wage. Those paychecks don’t line up well with $650,000 home prices, especially when rents track those same values.

Who gets squeezed—and how

For people whose incomes are rooted here, the affordability gap shows up in three main ways: they can’t buy, they struggle to rent, or they leave.

On the ownership side, the ladder from renting to buying is badly broken. When prices sit near 9 times the median income, even disciplined savers have a hard time keeping up; the down payment target keeps moving faster than their bank account balance. The HAI of 38.1 for first‑time buyers is a statistical way of saying what many renters already feel: the door to ownership is mostly closed unless you bring outside money with you.

In the rental market, the same forces play out in a different form. As more equity‑rich buyers and second‑home owners compete for a small pool of units, the average advertised rent climbs into the low 2,000s per month. For households earning what local service, care, or trades jobs pay, that often means overcrowding, doubling up with family, living in older units that never made it onto official listings, or carrying unsustainable rent burdens.

The third path is exit. Demographically, Eastern Jefferson County has become the oldest part of the state’s oldest county, with a median age near 60, a very high share of residents 65 or older, and a small share of children and teens. Deaths now outnumber births each year, so all net population growth comes from people moving in rather than being born here. In that context, every priced‑out teacher, nurse, bartender, or contractor who leaves and is replaced by a retiree or remote worker nudges the community a little older and a little wealthier.

The jobs-to-housing ratio captures this shift in a single snapshot. A healthy, employment‑centered community typically has somewhere between 0.75 and 1.5 jobs per housing unit. Eastern Jefferson County sits well below that, with roughly one job for every two housing units, which is consistent with a place oriented around retirement, second homes, and imported income rather than one where most residents work where they live.

STRs, second homes, and the nuance behind the blame

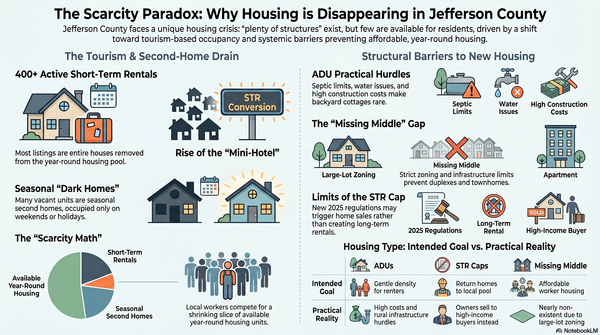

Short‑term rentals (STRs) and second homes are part of this story, but not in the neat cause‑and‑effect way they’re often portrayed. County and market data suggest there are roughly 400 active STRs in Jefferson County, generating something on the order of 17.5 million in gross revenue each year. About three‑quarters of those listings are entire homes, so each one of those units is not available as a year‑round rental or ownership opportunity for a local household.

In response, the county adopted new rules in 2025 that cap STRs at 4 percent of the housing stock per ZIP code in unincorporated areas, limit operators to one permit, and require annual life‑safety inspections and licenses. On paper, that should slow further conversion of primary housing into STRs. In practice, enforcement has lagged: hundreds of unpermitted STRs were still operating as of early 2026, and only a small share of non‑compliant operators had been brought into the system.

At the same time, STRs play real roles in the local housing and visitor ecosystem. They run at high occupancy, house traveling nurses and tradespeople, give families a flexible place to land between leases or during remodels, and support the tourism economy that many local businesses depend on. Conforming STRs collect lodging tax, which flows into the county’s Lodging Tax Advisory Committee fund and helps pay for tourism marketing, events, and visitor‑serving facilities.

On the ground, the friction often lies less in the concept and more in the implementation. I see that up close as both a local broker and a short‑term rental operator. I’ve paid my fees, submitted my paperwork, and passed my inspections—and nearly a year later, I still don’t have my permit. For me, it’s a good example of how this market feels for people trying to work within the rules: the issue isn’t simply “too many STRs,” it’s a system that struggles to process permits, enforce limits on bad actors, and give clear, timely answers to people who are trying to do things right.

Second homes add another layer. A large share of vacant housing units in unincorporated Jefferson County are classified as seasonal or recreational. That translates into a double‑digit percentage of all housing units effectively being removed from the year‑round housing pool, many of them in the most desirable waterfront and view locations. Those homes still rely on local road, fire, and utility systems, but they don’t house the workforce that keeps those systems functioning.

What the affordability gap is turning us into

Put all of this together—prices near $650,000, incomes near $74,000, HAI in the 50s overall and 30s for first‑time buyers, a buyer pool dominated by retirees and amenity migrants, a jobs‑to‑housing ratio under 0.5—and you start to see the outline of a different kind of community than the one many longtime residents remember.

Eastern Jefferson County still depends on teachers, nurses, sheriff’s deputies, hospitality workers, tradespeople, and caregivers. The restaurants are still open, the schools still need staff, the hospital still runs 24/7, and the mill still turns out product. But the housing market that serves those jobs is increasingly a byproduct of other forces: retirement migration, second homes, remote work, and investment income earned elsewhere.

For many people whose incomes are rooted in this place, the choice is narrowing to something like this:

- Stretch to buy at the outer edge of what a lender will allow and hope nothing goes wrong.

- Compete for a shrinking pool of rentals and accept a rent burden that leaves little margin for savings.

- Commute from farther away, or quietly leave for a place where local work and local housing are still in the same ballpark.

Those are affordability stories, not just policy stories. In Part 5, we’ll turn to the other side of the equation: how specific decisions—and non‑decisions—in policy and planning helped create a market where outside money sets the price of admission, and why the system has been so slow to change course.